Revelation report

Sagarika Mishra does not work to possess, request, very own shares inside otherwise discover financing off any business otherwise organisation that would make the most of this short article, possesses expose zero associated associations past the academic conference.

People

If you are paying only $step 1 a day even more on the financial, you might deceive the newest bank operating system and you will slice the time and energy to pay your house financing out-of two decades to simply 5 years.

Audio too good to be true? Naturally it is. But one has not averted individuals proficient at funds from claiming which inside good TikTok films which is garnered countless viewpoints and you can sparked all those other finfluencers so you can amplify its claims.

According to the clips: How come banks would like you to pay notice monthly is really because it believe in anything named material desire. But if you pay the lender $step one every day you pays a massive fat no inside the attention.

The fresh new videos goes on to state mortgage try an effective Latin term, together with cause they eliminated training Latin within the colleges is basically because they don’t want anybody finding out how the new banking system functions.

Should this be an excellent conspiracy principle, it’s because its. As with any conspiracy theories, this option try a great falsehood constructed on a few grain away from specifics, capitalizing on man’s ignorance regarding challenging issues.

What exactly is compound notice?

Say you place $step one,000 in a family savings one will pay ten% appeal. Pursuing the first 12 months, you would enjoys $1,100 ($step 1,000 + $100 when you look at the appeal). At the conclusion of another year there are $step 1,210 ($step one,100 + $110 when you look at the notice). At the end of the 3rd 12 months there’ll be $step one,331 (step 1,210 + $121 when you look at the focus). The eye ingredients.

What if you’ve lent $1,000 within an excellent 10% annual interest? Assuming you create zero money, after 12 months you will are obligated to pay $step 1,100 ($1,000 + $100 in the attention), immediately following a couple of years $1,210 ($1,100 + $110 inside focus), and you may after three years $step one,331 ($1,210 + $121 when you look at the attention). Again, the interest ingredients.

How to avoid material notice

To reduce the degree of substance appeal you have to pay, there is you to definitely effective method: pay back the mortgage as quickly as you could potentially.

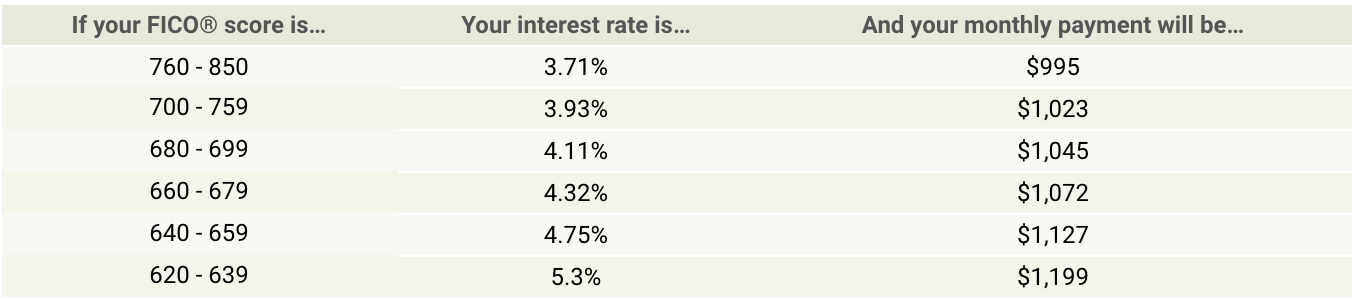

Consider an example just as the circumstance said regarding the TikTok clips home financing that have financing name off two decades. To make the maths effortless, can you imagine the borrowed funds is actually for $500,000 having good 5% rate of interest. To invest it off on the allotted day will require month-to-month costs of around $3,3 hundred or $39,600 per year.

Now let’s consider what would happen if the, in the place of paying $3,three hundred thirty days, your paid $1,650 two weeks. At first glance which may seem like the same, it actually.

Inside the a-year you can find one year, but twenty six fortnights (given that just February is precisely five weeks’ long). Investing 50 % of their month-to-month cost all 14 days will mean you pay $42,900 annually, as opposed to $39,600.

Whenever you afford to accomplish that, it needs simply 17 ages and 6 months to settle the loan, and you will pay in the $41,750 quicker attention. Another chart depicts it.

What exactly on spending everyday?

There isn’t any miracle secret to help you finishing material attract. The next chart reveals just what an additional $1 day carry out reach with your hypothetical $500,000 financing.

In place of taking 2 decades to repay the borrowed funds, it requires loans Ophir 19 years and you can 9 months. Might save your self from the $5,470 from inside the attract (using on the $286,480 as opposed to $291,950).

To repay the loan inside 5 years, just like the reported, would want paying an extra $201 a day or just around $113,220 a year as opposed to $39,600.

There are not any wonders cheats

You can find techniques to alter your loan conditions, including refinancing whenever rates of interest is actually decreasing, otherwise using a counterbalance account facility where talking about given.

The only means to fix minimise compound attract on the financial is to pay off your debts as fast as you can be.

Prior to you will do, speak to your bank if the there are fees in it for folks who generate most repayments towards your mortgage.

As an example, when you yourself have a partially otherwise totally fixed mortgage, there is certainly a limit precisely how much most you happen to be acceptance to settle annually in the place of penalty.

Such penalties developed to pay the financial institution into the loss of interest earnings it can have received in the event the borrower had continued and also make regular money along side complete mortgage identity.